Texas housing sales slowed in August, trending downward as supply remained constrained. Despite lowered mortgage interest rates, double-digit home-price appreciation chipped away at housing affordability. Elevated levels of demand persisted as homes averaged less than a month on the market. On the supply side, single-family housing permits declined for the third consecutive month, and housing starts decelerated even as pandemic effects on the lumber supply improved, causing a precipitous fall in prices; other material costs remained elevated. The historically low level of inventory available for sale is the greatest challenge to Texas’ housing market. The state’s diverse and expanding economy, favorable business policies, and steady population growth, however, support a favorable outlook.

Supply1

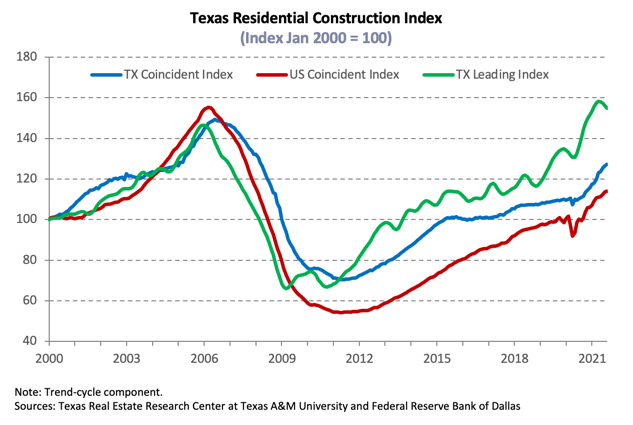

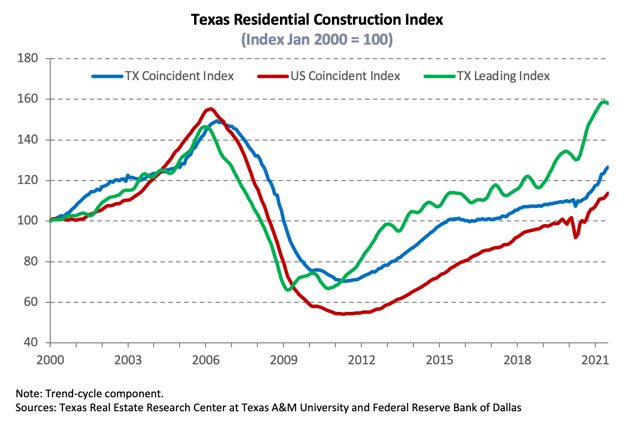

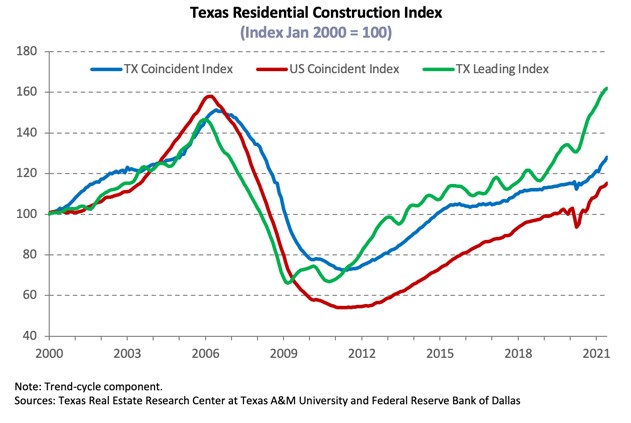

The Texas Residential Construction Cycle (Coincident) Index, which measures current construction activity, elevated nationally and within Texas due to improved industry wages and construction values, while employment flattened during August. The Texas Residential Construction Leading Index, however, decreased as weighted building permits flattened and residential starts decreased, while the ten-year real Treasury bill increased. The leading index trended downward, signaling a potential slowdown in future activity. Dallas-Fort Worth (DFW) and Austin’s weighted building permits reflected the statewide fluctuations as residential starts decreased in both metros. DFW leading index decreased, while Austin’s metric flattened. Houston and San Antonio’s indexes, however, suggested steady construction in the coming months as building permits and residential starts increased.

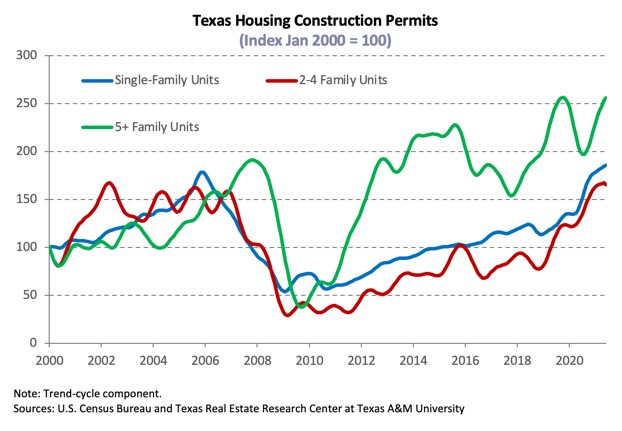

Single-family construction permits declined for the third consecutive month, falling 7.9 percent in August. Houston topped the national list for six straight months with 4,202 nonseasonally adjusted permits despite registering a seasonally adjusted decrease. DFW posted a double-digit monthly decline to 3,389 permits. Meanwhile, Austin and San Antonio issued 1,947 and 1,279 permits, respectively. On the other hand, Texas’ multifamily sector registered a steep expansion as issuance shifted from two-to-four units to five-or-more units. The metric accelerated 41.0 percent on a monthly basis and 22.6 percent year to date (YTD) relative to the same period last year.

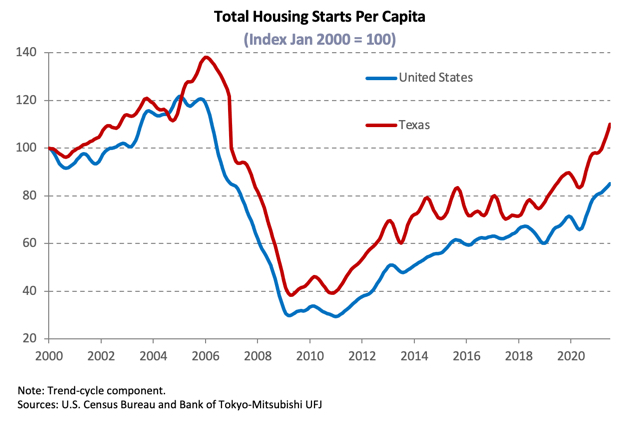

Despite strengthening economic conditions and ample housing demand, total Texas housing starts remained unchanged even as lumber prices declined 19.5 percent in August. Single-family private construction values, however, declined 6.6 percent in real terms as the metric trended downward in Texas’ major metros. The majority of the statewide reduction was attributed to the steep plummet in DFW values during August.

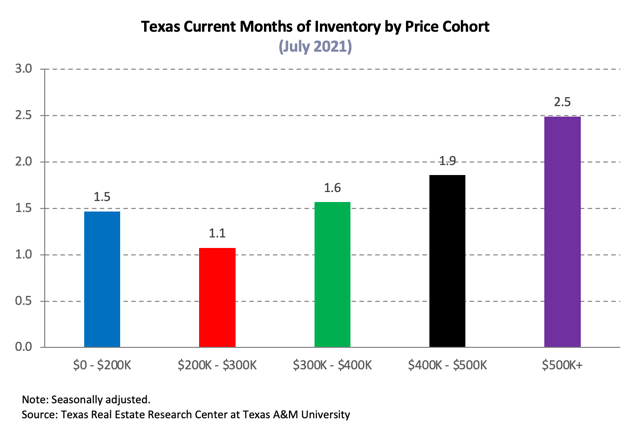

Texas’ months of inventory (MOI) ticked up slightly to 1.5 months as sales activity and new listings decreased. A total MOI around six months is considered a balanced housing market. Supply improved across all price cohorts for the third consecutive month. Inventory for homes priced between $300,000 and $399,000, the most expansive price, grew to 1.6 months, while the MOI for luxury homes (those priced more than $500,000) increased to 2.5 months.

Inventory in the major metros increased, except in North Texas, where MOI declined slightly to 1.2 months in Dallas and Fort Worth. Supply remained the most constrained in Austin at 0.9 months. San Antonio inventory expanded to 1.7 months while Houston’s MOI expanded to 1.8 months. Although overall supply increased in August, limited inventory persisted as a major headwind to the health of Texas’ housing market.

Demand

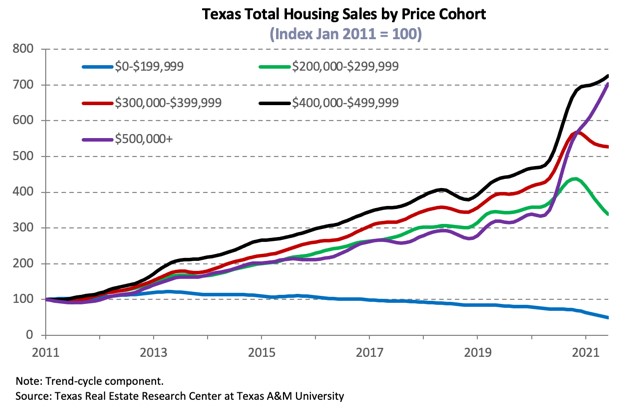

Total housing sales decreased 0.9 percent in August for the third consecutive month despite lowered mortgage interest rates. The slowdown was attributed to record low activity for homes priced less than $200,000 due to dwindling inventories. On the other hand, the number of homes sold priced more than $400,000 reached an all-time high.

Housing sales decreased at the metropolitan level except in North Texas. Reflecting statewide fluctuations across the price spectrum, San Antonio total sales declined 1.8 percent. In Houston, the metric dropped 1.5 percent, while activity in Austin contracted 0.8 percent. On the other hand, sales accelerated in Dallas and Fort Worth, increasing 1.1 and 4.1 percent, respectively, amid strong gains for homes priced between $400,000 and $499,000.

Texas’ average days on market (DOM) fell to a record-breaking 27 days, confirming robust demand and that the YTD decrease in sales was due to restricted inventory. Austin’s DOM increased slightly to 18 days, while the average in North Texas decreased, selling after an average of just 20 days in Fort Worth and 21 days in Dallas. San Antonio and Houston’s metric registered declines but hovered closer to the statewide average, falling to 26 and 29 days, respectively.

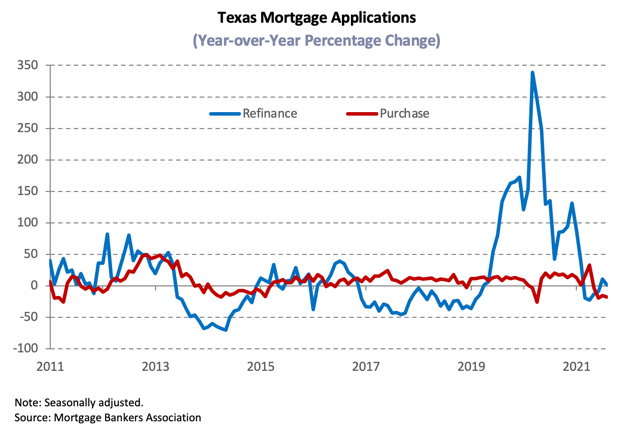

Amid low expectations of additional fiscal and monetary stimulus, economic growth forecasts for the rest of the year cooled as the initial and strongest stage of recovery likely reached its peak, and inflation pressures are believed to be temporary. The ten-year U.S. Treasury bond yield ticked down for the fourth consecutive month to 1.3 percent2, while the Federal Home Loan Mortgage Corporation’s 30-year fixed-rate fell to 2.8 percent. The median mortgage rate for the typical Texas homebuyer decreased in July3 to 3.1 and 3 percent for GSE and nonGSE loans, respectively. As mortgage rates dropped, Texas home-purchase applications increased over the past two months but fell 17.5 percent YTD. Refinance applications improved on a monthly basis yet were still down 12.2 percent over the same period. The annual decreases were likely due to baseline effects after a surge of remodeling and refinancing in 2020. Lenders adding more requisites, and the shrinking pool of households able to refinance is likely impacting refinance activity as well. (For more information, see Finding a Representative Interest Rate for the Typical Texas Mortgagee.)

In July, the median loan-to-value ratio (LTV) constituting the “typical” Texas conventional-loan mortgage dropped from 85.8 a year ago to 84.1. The debt-to-income ratio (DTI) was down from 36.0 to 35.8, while the median credit score increased only three points in the last year to 752. The LTV GSE borrowers also decreased from 86 last July to 85.4; however, DTI grew from 35.5 to 35.8. Overall improved credit profiles reflected the fact that only the most qualified housing applicants were able to outbid their competition for their desired homes amid exceptionally tight inventories and robust demand.

Prices

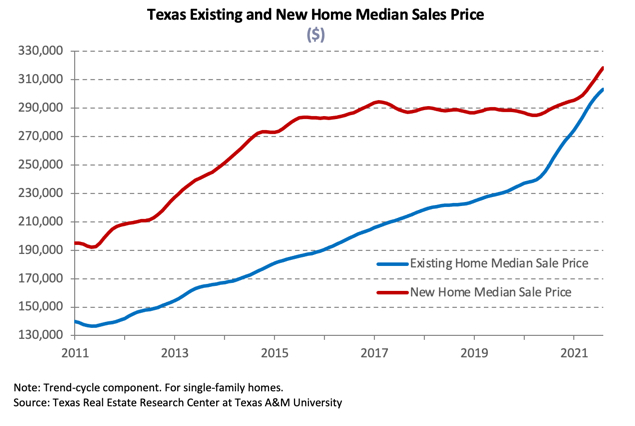

The ongoing shift in the composition of sales toward higher-priced homes due to constrained inventories at the lower end of the market supported home-price appreciation. The Texas median home price rose for the eighth consecutive month, accelerating 1.2 percent on a monthly basis and 16.8 percent YOY to a record-breaking $305,400 in August. The share of luxury homes sold in Austin continued to expand, contributing to the 34.6 percent YOY surge in the median price ($464,900). The Dallas metric ($374,200) increased 18.4 percent while annual price growth in Fort Worth ($312,600) shot up to 20.1 percent. Houston’s ($301,700) and San Antonio’s ($289,500) metrics elevated 15.5 and 16.1 percent, respectively.

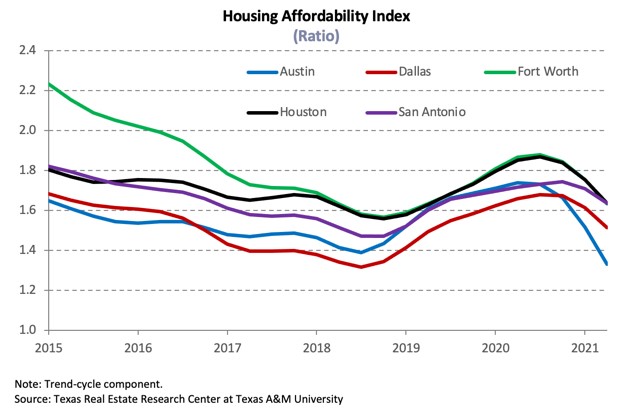

The Texas Repeat Sales Home Price Index accounts for compositional price effects and provides a better measure of changes in single-family home values. Texas’ index corroborated substantial and unsustainable home-price appreciation, accelerating 18.3 percent YOY. At the metropolitan level, the repeat sales index slowed in the major metros, except Houston, as annual price growth reached a peak. The metric decelerated 38.5 percent in Austin, followed by North Texas with 23 and 20.3 percent home-price appreciation in Dallas and Fort Worth, respectively. San Antonio posted an 18.1 percent annual hike, while Houston’s index accelerated 15.2 percent. Increasing home prices pressure housing affordability, particularly in an environment of low real wage growth.

Single-Family Forecast

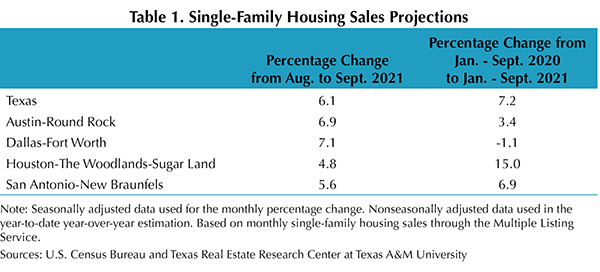

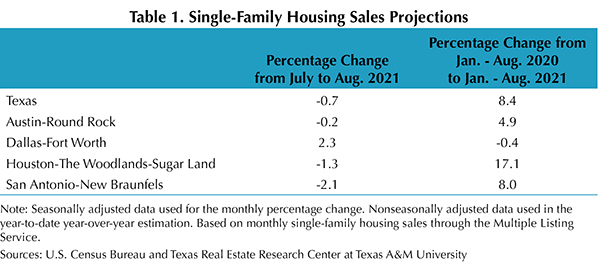

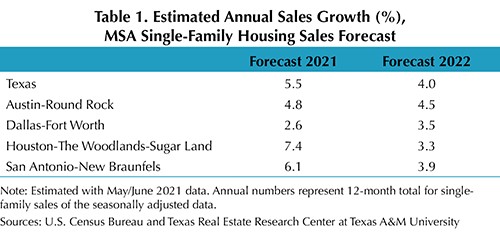

The Texas Real Estate Research Center projected single-family housing sales using monthly pending listings from the preceding period (Table 1). Only one month in advance was projected due to uncertainty surrounding the COVID-19 pandemic and the availability of reliable and timely data. Texas sales are expected to recover 6.1 percent in September after three consecutive monthly declines. The metric is estimated to rebound 6.9 and 5.6 percent in Austin and San Antonio, respectively, with additional increases of 7.1 percent in DFW and 4.8 percent in Houston. Sales through September 2021 should accelerate relative to the same time period in 2020. On the supply side, inventories reached a trough in May 2021 and should improve in the coming months. Listings seem to have reached a trough and are rising, easing some of the price pressures. (For more information, see the 2021 Mid-Year Texas Housing & Economic Outlook.)