All measurements are calculated using seasonally adjusted data, and percentage changes are calculated month-over-month, unless stated otherwise.

In a sign of stabilization, Texas’ home sales rose significantly in December to deliver a strong fourth-quarter finish going into 2025. Rising sales were seen broadly across all major markets (Austin, Dallas-Fort Worth, Houston, and San Antonio) as well as in smaller markets outside the Big Four. 4Q2024 marks the first time since the beginning of the housing recession that home sales rebounded strongly to end the year with double-digit year-over-year (YoY) growth.

Home prices remained steady and ended the year higher than a year ago. Positive year-end trends also captured rising new listings and rising inventory amid strong fourth-quarter sales momentum. Mortgage rates remained high going into 2025 despite a third round of interest rate cuts by the Federal Reserve in December. Mortgage rates are likely to stay near where they are during persisting signs of market jitters over inflationary pressure.

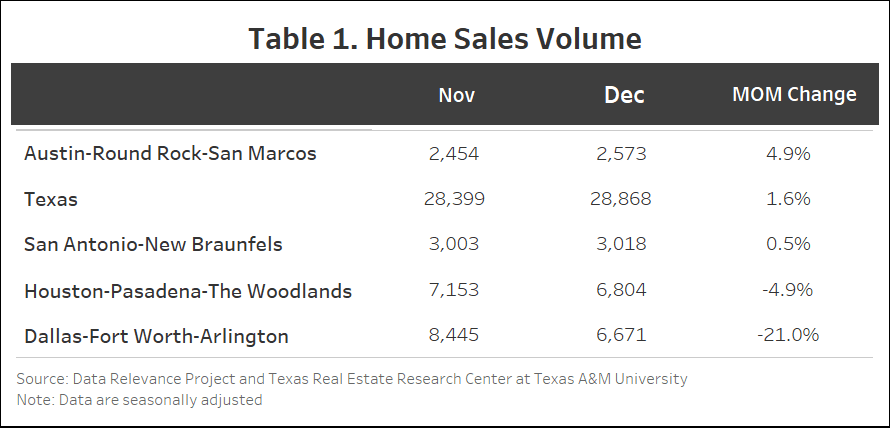

December’s Seasonality: Small Market Sales Up, Big Four Sales Down

In most years, sales rebound in December after a weak November, and this year is not any different. What was different was that December’s seasonal rebound was driven by strong sales in markets outside the Big Four. Statewide, there were 28,868 home sales in December, up 1.6 percent from November. In the major metros, aggregate sales volume (19,066) declined by 9.4 percent, driven by a 21 percent drop in DFW and a 4.9 percent drop in Houston. Sales were up 4.9 percent in Austin and 0.5 percent San Antonio. Outside the major markets, total home sales (9,802) surged 33.5 percent from November (Table 1).

First Positive YoY Sales Since 2022

Total statewide home purchases were up 10.7 percent from a year ago, marking the first time since the 2022 housing recession that sales volumes came in higher than the year before. These strong fourth-quarter sales were broadly seen across various markets. In the Big Four, was Austin saw 7.6 percent sales growth, DFW 16.4 percent, Houston 16.5 percent, and San Antonio 8.2 percent. Home sales were up an average of 6.7 percent in smaller markets.

Positive Trends in New Listings and Inventory

Statewide new listings were up slightly in December on a month-over-month (MoM) basis. Among the Big Four, new listings rose 2.7 percent in Austin, 2.6 percent in San Antonio, and 1.6 percent in Dallas, but declined in Houston by 2.4 percent. On a YoY basis, new listings were up 7.6 percent statewide, 7 percent in Austin, 10.8 percent in DFW, 14.9 percent in Houston, and 8.4 percent in San Antonio.

During December, statewide average days on market (DoM) was 63 days, comparable to the pre-pandemic turnover pace. Average DoM was 58 days in DFW, 77 days in Austin, 53 days in Houston, and 75 days in San Antonio.

At year-end, statewide active listings totaled 123,364, slightly lower than the previous month. Austin’s MoM decline (12.3 percent) was its slowest pace of MoM decline for a December since 2021. Active listings were down slightly in San Antonio (1.5 percent) and DFW (1.4 percent). Houston’s active listings were relatively unchanged in December.

Interest Rates Remain High During Inflation Concerns

In December, the average yield on the ten-year U.S. Treasury bond increased by 3 basis points to 4.39 percent despite the Fed cutting its policy rate target by another 25 basis points. Inflation has remained persistently above the Fed’s 2 percent target, and the December Consumer Price Index (CPI) data showed signs of re-acceleration. The Freddie Mac Primary Mortgage Market Survey’s 30-year fixed-rate mortgage ended December at 6.85 percent, up 16 basis points higher than at the start of the month.

New-Home Starts Increased

Statewide, building permits increased a sharp 17.7 percent MoM in December. Newly authorized permits surged 24.7 percent in DFW, while Houston and San Antonio maintained a modest upward trend, rising 5.8 percent and 2.5 percent, respectively. Building permits were relatively flat in Austin, down 1.7 percent.

Seasonally adjusted statewide single-family starts increased 9 percent MoM to 14,207 units. Houston and DFW had the highest increases at 14.4 percent (4,491) and 11.6 percent (3,670), respectively. New housing starts were up 8.4 percent (1,567) in Austin. Despite a small positive increase in building permits, San Antonio’s new single-family starts (802) dropped 14.8 from the previous month.

The state’s total value of single-family starts climbed from $29.8 billion in December 2023 to $40 billion in December 2024.

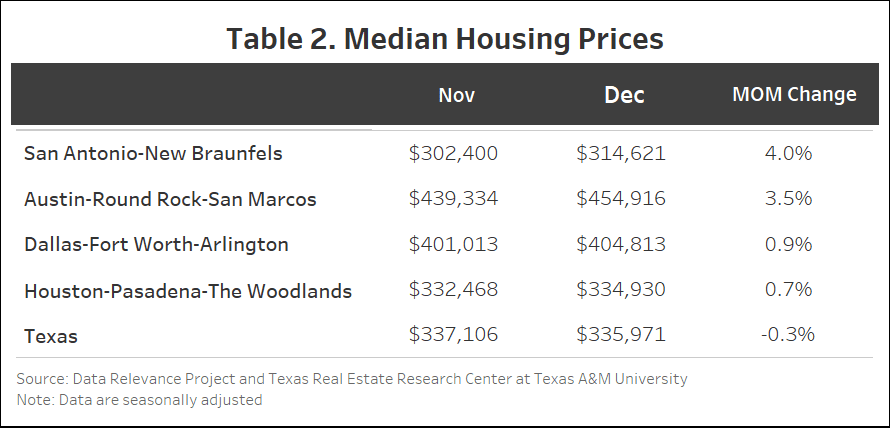

Texas HPI Up 2.1 Percent

Texas’ median sales price was $335,971 in December, a 0.3 percent MoM drop (Table 2). San Antonio was up 4 percent to $314,621, Austin 3.5 percent to $454,916, DFW 0.9 percent to $404,813, and Houston 0.7 percent to $334,930.

The Texas Repeat Sales Home Price Index, which more accurately captures home price change over time than median sales price, fell 0.1 percent month over month in December but increased 2.1 percent from a year ago.

Source: Texas Housing Insight | December 2024 | Texas Real Estate Research Center – By Yanling Mayer, Joshua Roberson, and Junqing Wu